The Anchorage Digital Prime Signal: What Skew, Wings, and the Term Structure Are Telling Us About Bitcoin and Its Adjacent Markets

Bitcoin options matured into an institutionally-driven market where the volatility surface carries real information that the spot price alone never can. In this piece, we read that surface and highlight what the Deribit, IBIT, and MSTR options markets are telling right now.

Options encode the market's forward-looking probability distribution. Skew tells you which direction the crowd is paying to protect against. The wings tell you how seriously they are taking the extremes. The term structure tells you when they expect things to get interesting. For participants who know how to read it, the volatility surface is night vision in a market most are still navigating in the dark.

This is especially true for Bitcoin, which now trades across three distinct options markets, each with its own participant base.

Deribit anchors the crypto-native flow. IBIT options have grown explosively and brought a new wave of mainstream institutional and retail participants into the fold. MSTR options attract an entirely different persona expressing a view on amplified Bitcoin through the instrument that has dominated the conversation in Bitcoin circles lately.

Reading all three together gives you something no single market can: a composite picture of how different types of Bitcoin believers are positioned right now.

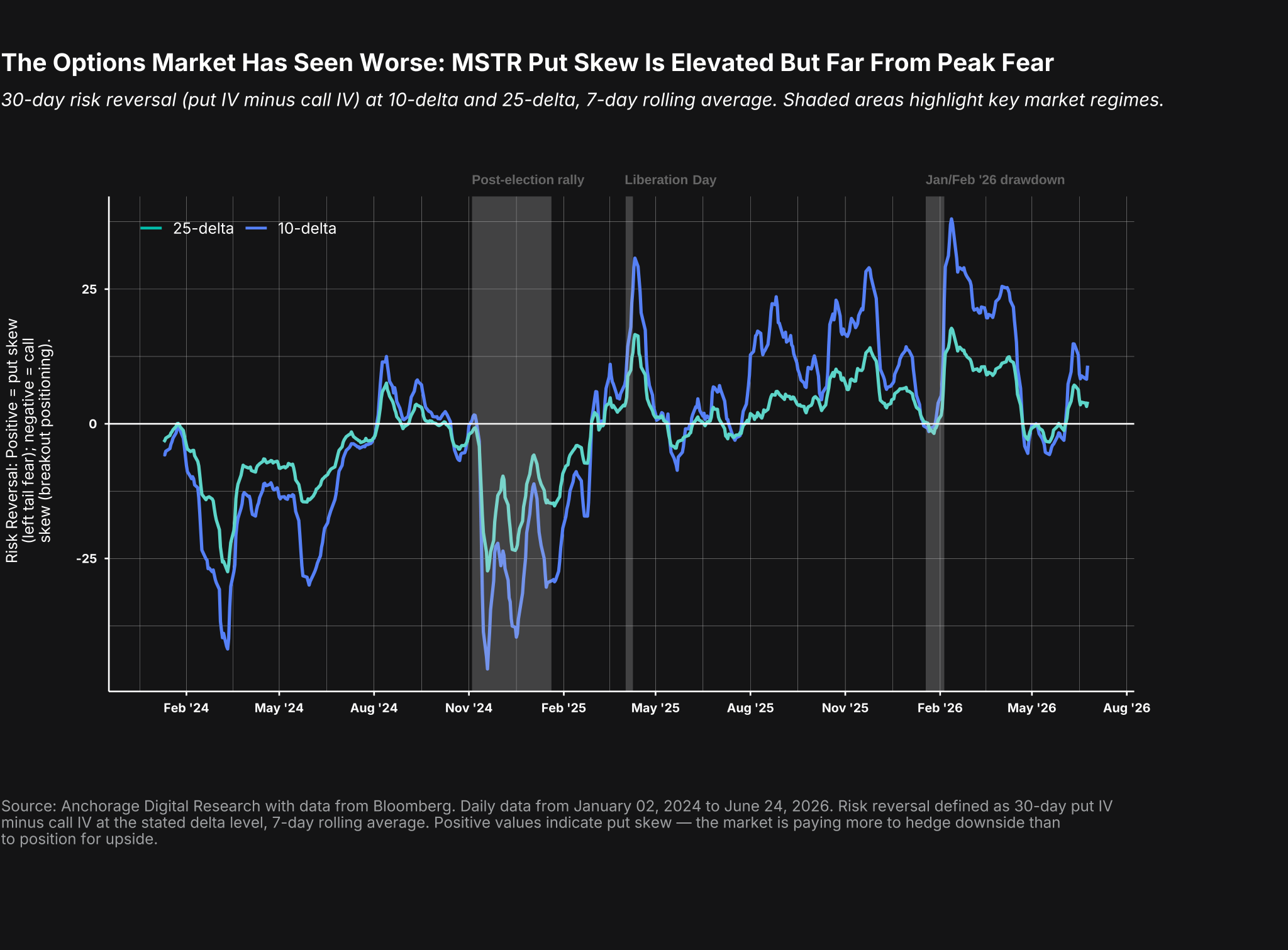

Signal 1: MSTR options are not flashing a crisis

One of the most actively debated questions in Bitcoin circles right now is whether the Strategy (MSTR) thesis is under meaningful structural stress. STRC, Strategy's flagship perpetual preferred stock instrument, hit a low of $82.53 on June 22, trading 17% below its $100 par value. While STRC’s price has recovered after this week’s 8-K showed a top-up of fiat reserves to $1.3 billion (10 months of interest), it is still pricing a 12.8% implied yield.

The options market offers a useful reality check. A risk reversal (RR) measures the difference between the implied volatility of out-of-the-money puts and calls at the same delta. In simple terms, how much more expensive it is to buy downside protection than to bet on upside. When put skew is elevated, the market is paying a premium to hedge against a left tail outcome. When call skew dominates the market is positioned for a breakout.

The chart below shows both the 10-delta and 25-delta risk reversals. While the former captures deep tail risk pricing and the latter reflects more moderate directional positioning, the message is the same: current MSTR put skew, while meaningfully positive and confirming that the market does see downside risk, is running well below past market corrections such as during Liberation Day in April 2025 and the Jan/Feb 2026 drawdown.

The 10-delta skew is particularly telling. It measures what the market is paying to hedge against a genuinely severe left tail outcome, the kind of non-linear downside that a forced deleveraging or NAV discount spiral would produce. That it remains well below its prior stress peaks suggests the options market is not pricing an existential scenario for MSTR. While both episodes were accompanied by sharp spot price dislocations and genuine panic in the options market, today's reading sits in elevated but not alarming territory. The options market has seen worse MSTR stress than this and current skew says the crowd is hedging but not fleeing.

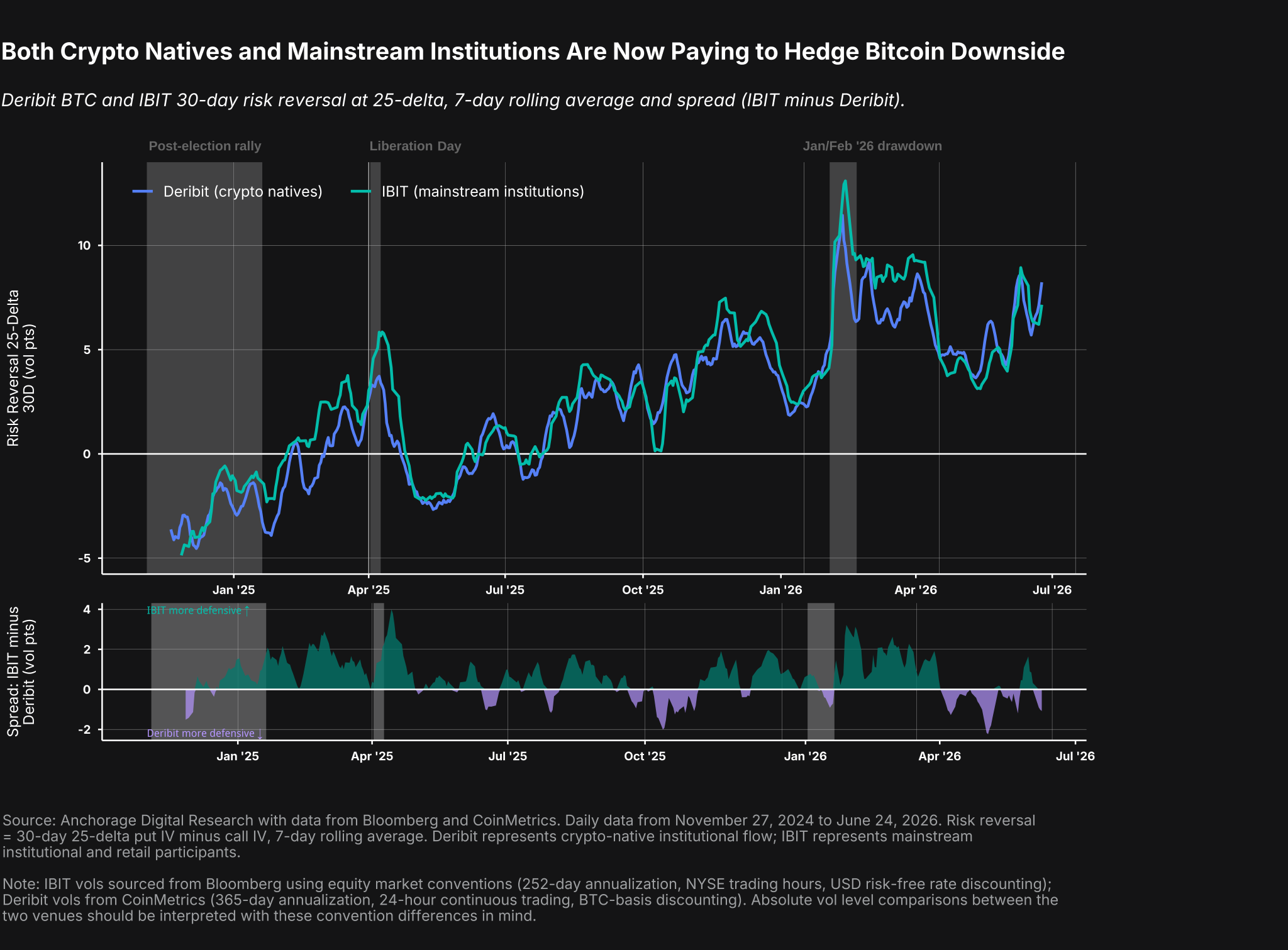

Signal 2: Both crypto natives and mainstream institutions are now paying to hedge bitcoin downside

BTC now trades across distinct options markets with fundamentally different participant bases, the most relevant of which are Deribit and the IBIT options. Deribit anchors the crypto-native flow: traders, funds, and market makers who have been navigating the volatility surface for years. IBIT options brought a new wave of mainstream institutional and retail participants into the fold, many of whom think in equity-market terms and arrived with a decidedly bullish disposition. Reading both together gives you a composite picture of how different types of Bitcoin believers are positioned.

The chart below tells a striking 18-month story. When IBIT launched during the post-election Bitcoin rally, both venues were in deep call skew as the mainstream crowd arrived reaching for upside, and crypto natives were positioned the same way. That consensus broke quickly. By early 2025 both markets had flipped to put skew, and they have largely stayed there ever since. IBIT has been skewed on 77.5% of trading days since launch. The current risk reversal at the 25 delta reading is at the 82nd percentile of IBIT's history and the 84th percentile of Deribit's five-year history, meaning both venues are at elevated defensive positioning levels.

The spread panel adds an important nuance. IBIT has been consistently more defensive than Deribit for most of its history, likely a structural feature of its non-24-hour trading window that leaves mainstream participants more exposed to overnight gap risk and pushes them toward maintaining a higher baseline of put protection. The more analytically interesting periods are when that relationship inverts and crypto natives become more defensive than mainstream institutions. Those red patches in the spread panel at the bottom have tended to mark good entry points for those looking for market capitulation.

The spread is currently near zero, meaning the two crowds are in rare alignment. For participants looking for a near-term entry signal, a negative reading of about two vol points would be worth watching. Historically those episodes have tended to mark the point where Deribit participants, who lead the defensive repositioning cycle, have fully priced in the downside and the mainstream crowd has yet to catch up. That divergence, when it appears, has been a more precise signal than either venue alone.

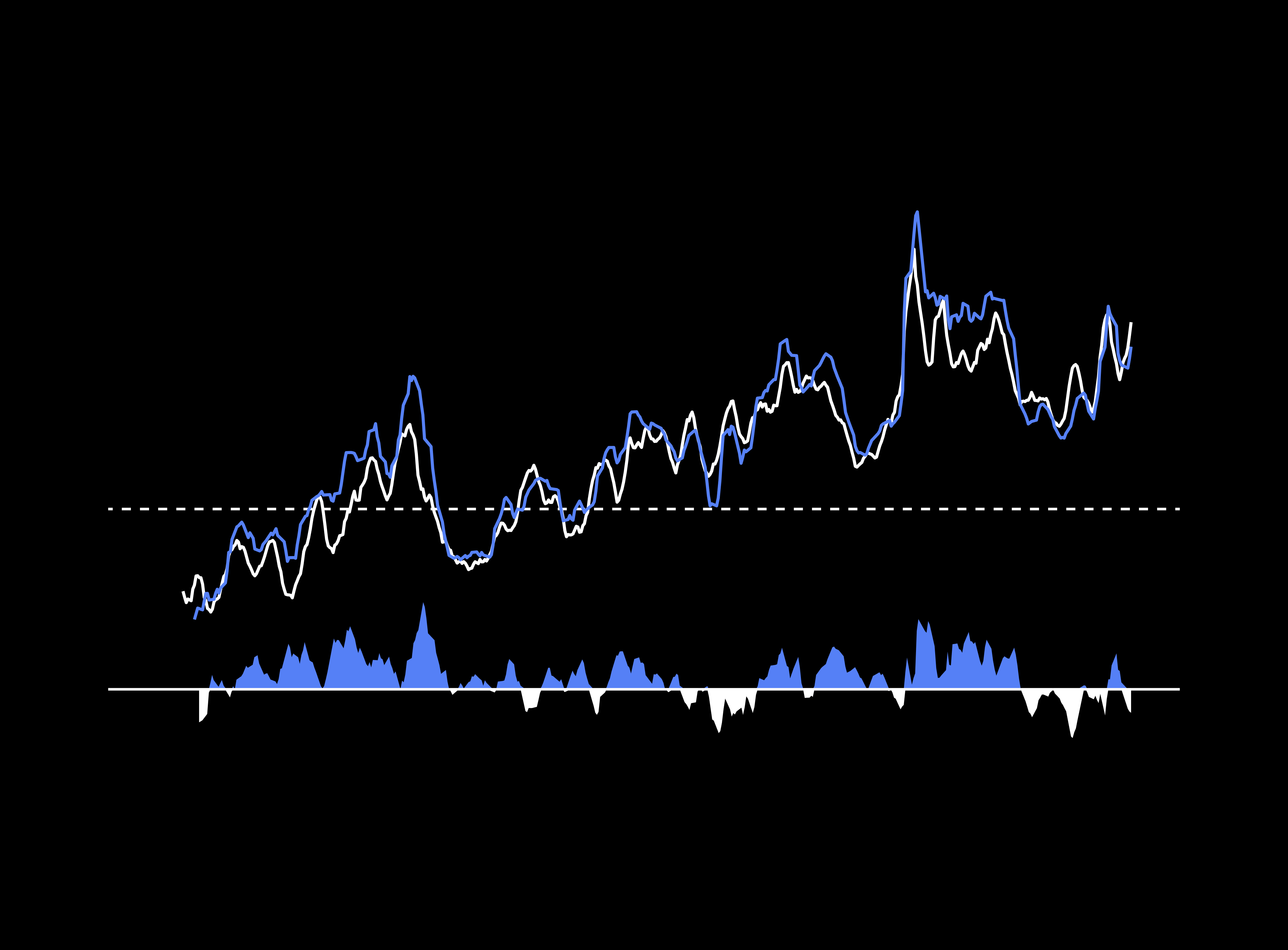

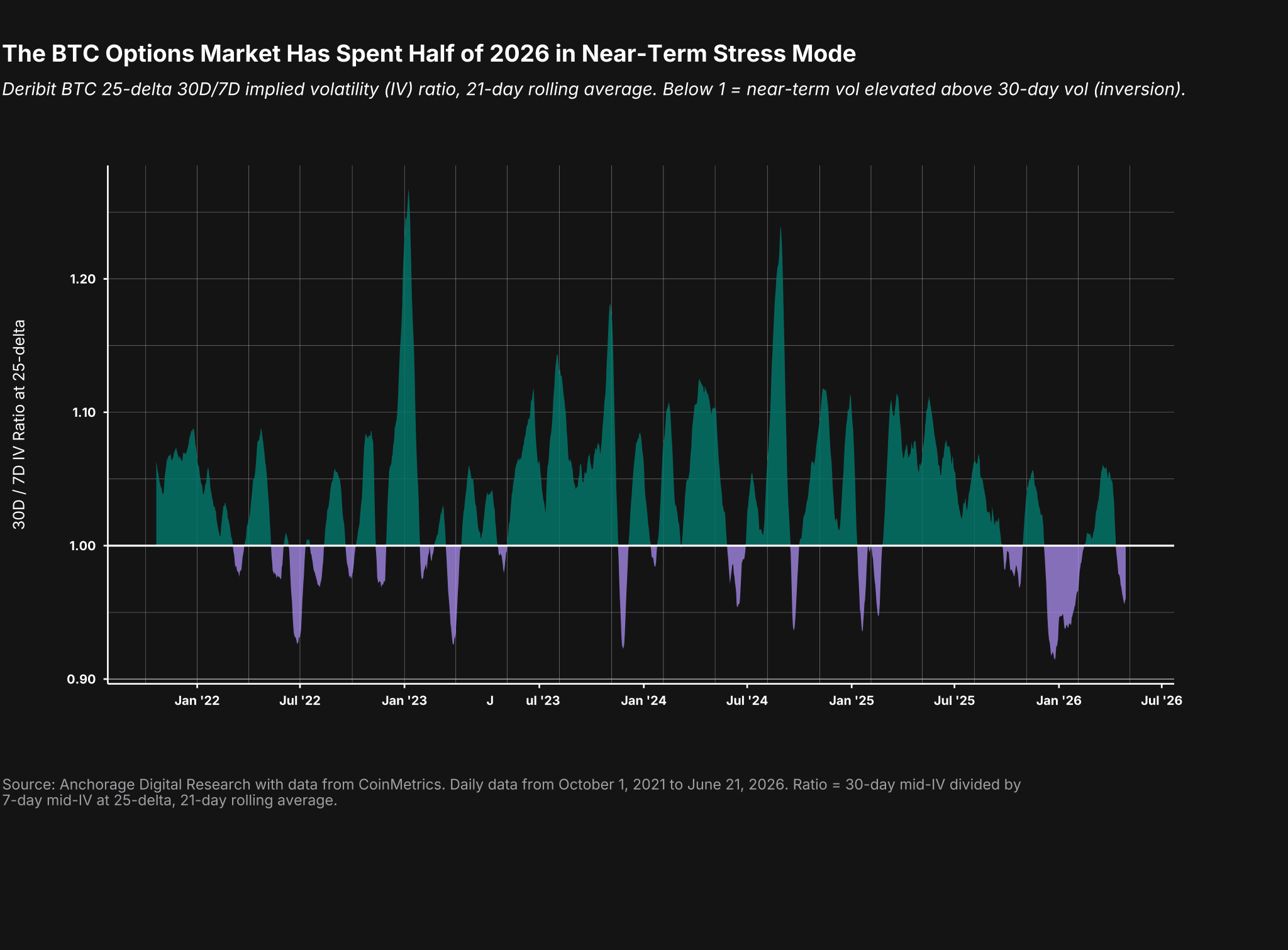

Signal 3: The BTC options market has been living in persistent near-term anxiety

The vol term structure is not the most watched corner of the options market but sometimes can be one of the most informative. In a normal options market, implied volatility increases with tenor, as one pays more for a 30-day option than a 7-day option because there is simply more time for things to not go according to plan. When that relationship inverts (for example: when 7-day vol exceeds 30-day vol) it signals that the market is more worried about what happens this week than what happens next month. That is an unusual state of affairs, and it tends to be episodic and short-lived.

In 2026, it has been neither. The Deribit BTC options market has spent nearly half of this year in inversion, as the 30-day to 7-day implied volatility ratio has been below 1.0 on 49% of trading days year-to-date. This compares to 19-21% in each of the three prior years. The only comparable period in our dataset is 2022, when the ratio was inverted 36% of the time during Bitcoin's most severe bear market. What we are seeing in 2026 is historically anomalous: a market that has been repeatedly caught off guard by near-term events and has repriced acute short-term uncertainty as the default rather than the exception.

The chart below makes this pattern visually clear. The green zones (periods when 30-day vol exceeds 7-day vol, the normal state) have been progressively compressed since 2025, while the red zones have become deeper and more frequent. The current reading, at the 7th percentile of the full five-year history, is not far from some of the most extreme inversion episodes on record.

What makes 2026 different from prior years is not the presence of inversion but its persistence.

In prior years, inversion was episodic and represented a specific event that triggered a short-dated volatility spike, the shock resolved, and the term structure normalized. In 2026, the shocks have kept coming from different directions: macro uncertainty around interest rates, growth, Federal Reserve independence, and other topics; geopolitical disruptions; and industry-specific catalysts including regulatory developments and the ongoing debate around Bitcoin treasury strategies. Each time the market has tried to normalize, a new source of near-term uncertainty has arrived. The result is a term structure that has spent nearly half the year inverted, in our view not because any single risk has been unusually severe, but because the rotation of risks has been unusually relentless.

The more important forward-looking signal is therefore not the inversion itself but its resolution. When the 30D/7D ratio recovers sustainably above 1.00, meaning when the market stops treating this week as more dangerous than next month, that normalization will signal that the rotation of near-term shocks has finally paused and the market is comfortable looking forward again. For participants waiting for a cleaner read on that risk, this is the indicator to watch.

What the vol surface is telling us

As the BTC market structure matures, the options market is becoming an increasingly important layer of analysis alongside the liquidity trends and leverage metrics that have traditionally dominated price action reading. Options encode forward-looking probability distributions that tell you not just where different personas are positioned but also how much conviction they have, how they are sizing their tail risk, and when they expect the next meaningful move.

Against that backdrop, none of the three signals we have examined today is flashing a sustainable directional trend. MSTR options are elevated but not at crisis levels. Both crypto-native and mainstream institutional participants are defensively positioned but not reaching for extreme tail protection. And the term structure inversion that has characterized 2026 reflects a market still searching for a stable regime rather than one that has found a direction.

The options market tends to flash those signals before spot does. The specific places I'm watching include the Deribit BTC 25-delta 30-day risk reversal compressing toward the 2-4 vol pt range, the 25-delta 30D/7D implied vol ratio recovering sustainably above 1.00, and the MSTR 10-delta 30-day skew normalizing from current elevated levels. For opportunistic entry points, I'll be looking for a combination of the IBIT-Deribit 25-delta 30-day risk reversal spread turning negative and the 25-delta 30D/7D ratio bottoming at or below 0.95.

Disclosures

Custody, settlement, staking, and governance services are offered through Anchorage Digital Bank National Association (“Anchorage Digital Bank”). Digital asset trading services are provided by Anchorage Hold LLC (“Anchorage Hold”). Agency trading services are offered in New York by Anchorage Digital NY, LLC. BitLicense #0000041. A1 Ltd. is a principal trading business. Anchorage Services, LLC (“Anchorage Services”) is an NFA-registered introducing broker, NFA ID No. 0532710. Anchorage Digital Bank, Anchorage Hold, and Anchorage Services are not registered with the SEC or any state authority as a broker or dealer and are not authorized to engage in the business of the offer, sale, or trading of securities. Anchorage Digital services are offered to institutions and certain high net worth individuals in limited circumstances. Certain trading services are designed and available only for institutions who meet eligibility requirements, including qualification as an Eligible Contract Participant (ECP) under the rules of the U.S. Commodity Futures Trading Commission. For institutions participating in custody, staking, or governance with Anchorage’s Singapore entity, those services are offered through Anchorage Digital Singapore Pte Ltd (“Anchorage Digital Singapore”). Anchorage Digital does not provide legal, tax, or investment advice or private banking services. There can be no assurance that any cryptocurrency, token, coin, or other crypto asset will be viable, liquid, or solvent. No Anchorage Digital communication is intended to imply that any digital asset services are low-risk or risk-free. Digital assets held in custody are not guaranteed by Anchorage Digital and are not subject to the insurance protections of the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC).

For institutions participating in custody, staking, or governance with Anchorage’s Singapore entity, those services are offered through Anchorage Digital Singapore Pte Ltd (“Anchorage Digital Singapore”), a major payments institution licensed by the Monetary Authority of Singapore.

Digital assets held in custody are not guaranteed by Anchorage Digital and are not subject to the insurance protections of the Singapore Deposit Insurance Corporation (“SDIC”). Anchorage Digital Singapore is not a member of the Singapore Deposit Insurance (“DI”) Scheme and assets are not subject to the protections enjoyed by depositors with DI Scheme member institutions.

Anchorage Digital Bank National Association offers fiat custody services through the use of an FDIC-insured, licensed sub-custodian.

This Stablecoin Rewards Program (the "Program") is offered by an entity separate from Anchorage Digital Bank, N.A. Stablecoins must be held with custody or wallet platforms offered by Anchorage Digital Bank National Association, Anchorage Digital Singapore Pte, Ltd., or Anchorage Innovations, LLC, in order to be eligible for rewards. This program is not offered by any of the aforementioned custody or wallet service providers. Please refer to the Stablecoin Rewards Program Terms & Conditions for all applicable terms and risks. By participating in the Program, participants acknowledge that they have read, understood, and agreed to be bound by this disclaimer and any other terms and conditions governing the Program. Information in this document is for general educational purposes only and eligibility limitations apply. This document is not intended to constitute an offer, solicitation, recommendation, investment, or any other advice on financial products. Availability is subject to jurisdictional limitations.

The Program is not subject to regulatory oversight in any jurisdiction. Participants in the Program acknowledge and understand that the Program is not regulated by any governmental authority. As such, there are no guarantees regarding the stability, security, or reliability of the Program. Participation in the Program carries inherent risks, including but not limited to the risk of loss of funds, lack of recourse in case of disputes, and potential volatility of a stablecoin's value. Participants are responsible for understanding and complying with all applicable laws, regulations, and requirements in their respective jurisdictions regarding the use, possession, and transfer of digital assets, including stablecoins. Nothing in the Program constitutes investment advice, financial advice, or any other form of professional advice. Participants should conduct their own research and seek appropriate professional advice before participating in the Program. Anchorage Digital Neo, Ltd. and its affiliates, officers, directors, employees, agents, and representatives shall not be liable for any losses, damages, liabilities, costs, or expenses arising out of or related to participation in the Program, regardless of the cause of action or legal theory asserted.

“Anchorage Digital Prime" is a trade name for a suite of digital asset products and services. It does not refer to any one specific legal entity. All services are provided by one or more of the specific Anchorage Digital entities. Custody, settlement, staking, and governance services are offered through Anchorage Digital Bank National Association (“Anchorage Digital Bank”). services are provided by Anchorage Hold LLC (“Anchorage Hold”). Agency trading services are offered in New York by Anchorage Digital NY, LLC. BitLicense #0000041. A1 Ltd. is a principal trading business. Anchorage Services, LLC (“Anchorage Services”) is an NFA-registered introducing broker, NFA ID No. 0532710. Anchorage Digital Bank, Anchorage Hold, and Anchorage Services are not registered with the SEC or any state authority as a broker or dealer and are not authorized to engage in the business of the offer, sale, or trading of securities. Anchorage Digital services are offered to institutions and certain high net worth individuals in limited circumstances. Certain trading services are designed and available only for institutions who meet eligibility requirements, including qualification as an Eligible Contract Participant (ECP) under the rules of the U.S. Commodity Futures Trading Commission. For institutions participating in custody, staking, or governance with Anchorage’s Singapore entity, those services are offered through Anchorage Digital Singapore Pte Ltd (“Anchorage Digital Singapore”). Anchorage Digital does not provide legal, tax, or investment advice or private banking services.

Find additional legal and compliance information at anchorage.com/legal.

About Anchorage Digital

Anchorage Digital is a global crypto platform that enables institutions to participate in digital assets through trading, staking, custody, governance, settlement, stablecoin issuance, and the industry’s leading security infrastructure. Home to Anchorage Digital Bank N.A., the first federally chartered crypto bank in the U.S., Anchorage Digital also serves institutions through Anchorage Digital Singapore, which is licensed by the Monetary Authority of Singapore; Anchorage Digital NY, which holds a BitLicense from the New York Department of Financial Services; and self-custody wallet Porto by Anchorage Digital. Anchorage Digital Bank also offers fiat custody services through the use of an FDIC-insured, licensed sub-custodian. Anchorage Digital is funded by leading institutions including Andreessen Horowitz, GIC, Goldman Sachs, KKR, and Visa, with a valuation of $4.2 billion. Founded in 2017 in San Francisco, California, Anchorage Digital has offices in New York, New York; Porto, Portugal; Singapore; and Sioux Falls, South Dakota. Learn more at anchorage.com, on X @Anchorage, and on LinkedIn.

This post is intended for informational purposes only. It is not to be construed as and does not constitute an offer to sell or a solicitation of an offer to purchase any securities in Anchor Labs, Inc., or any of its subsidiaries, and should not be relied upon to make any investment decisions. Furthermore, nothing within this announcement is intended to provide tax, legal, or investment advice and its contents should not be construed as a recommendation to buy, sell, or hold any security or digital asset or to engage in any transaction therein.

Anchorage Digital Bank National Association offers fiat custody services through the use of an FDIC-insured, licensed sub-custodian.